[ad_1]

The past week marked one of the most decisive turns for markets in months. Fed Chair Jerome Powell’s Jackson Hole speech was the clear catalyst, tilting Fed closer to easing and sparking a rally that lifted Wall Street to new highs. Dollar, by contrast, tumbled sharply.

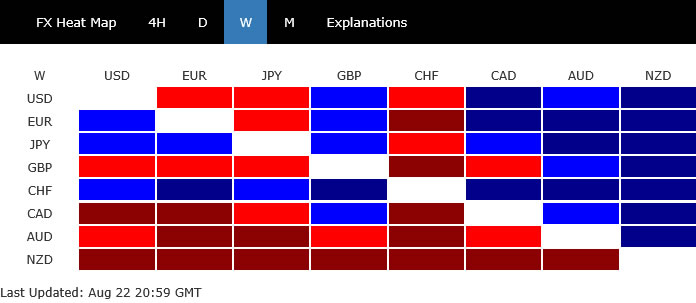

On the surface, Swiss Franc and Yen came out on top in weekly FX performance, supported early by risk aversion but now facing pressure as Fed easing hopes drive global stocks higher. Euro also gained, bolstered by resilient Eurozone data that hinted the bloc may be handling trade headwinds better than feared.

On the other side, Kiwi was weighed down by RBNZ’s dovish cut, which left the door wide open for more easing both this year and next. Aussie tracked lower in sympathy, though its fate hinges on whether it can decouple from its weaker neighbor. Sterling also lagged despite firmer inflation readings.

Dollar ended in the middle of the pack, along with Loonie. But the greenback’s late-week slide suggests this is more than just a temporary adjustment. Selling momentum is likely to extend, at least for the near term, until incoming data like non-farm payrolls give fresh guidance.

Powell Tilts Fed Toward September Cut, Yet Consensus Still Fractured

US equity markets roared higher on Friday as investors embraced Fed Chair Jerome Powell’s Jackson Hole speech as a dovish pivot. DOW jumped 846 points, or 1.89%, to a record close at 45,631.74. S&P 500 rose 1.52%, while NASDAQ gained 1.88%, with tech and cyclicals leading broad-based gains. Currency markets told the same story in reverse. Dollar was dumped across the board, extending sharp losses as traders repriced the Fed outlook.

The key line was Powell’s acknowledgment that “with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.” Markets interpreted this as the clearest sign yet that Fed is edging toward rate cuts.

Powell’s wording suggests that Fed has effectively looked through tariff uncertainty and is now more concerned about the slowdown in the labor market. In effect, the central bank may have shifted from a “no move unless there is a surprise” stance in July to a “cut unless there is a surprise” stance heading into September.

Fed fund futures quickly reflected the shift in tone. Probability of a September cut, which had dipped near 70% earlier in the week following robust US PMI data, rebounded to around 85%. While still shy of the 90%-plus odds seen a week ago, the repricing was swift and decisive after Powell’s speech.

That said, Powell’s view is not necessarily the consensus within Fed. Hawks have continued to push back against market optimism. Cleveland Fed President Beth Hammack reiterated that if the FOMC were meeting tomorrow she “would not see a case for reducing interest rates,” citing persistently high inflation that’s “trending in the wrong direction”.

Kansas City Fed President Jeffrey Schmid voiced similar caution, stressing that with inflation still closer to 3% than 2% and the labor market stable, there was “no rush” to cut. He said policymakers would need “very definitive data” before justifying a move.

This hawkish resistance means any September rate cut is likely to be accompanied by a split vote. Powell may have nudged the Fed toward easing, but consensus remains elusive. The committee is far from united on whether inflation progress is sufficient to justify a pivot.

Beyond September, the path looks even less certain. Unless incoming data — particularly the next NFP and CPI releases — shift hawkish views, the Fed is unlikely to commit to an aggressive easing cycle. A cautious, data-dependent path remains the most likely scenario.

For now, markets are content with Powell’s hint. Wall Street has surged to fresh records and the Dollar has slumped, but the real test will be whether upcoming data give Fed hawks reason to relent, or whether they push back hard enough to temper the market’s enthusiasm.

DOW Hits Record, Dollar Index Vulnerable

Powell’s dovish shift at Jackson Hole not only triggered a powerful rally in equities and a broad Dollar selloff but also set up key technical developments across major benchmarks. The breakout in DOW and the vulnerability in Dollar Index are now reinforcing the macro narrative, showing that the policy pivot is translating directly into decisive market momentum.

DOW finally cleared the critical 45,073.63 resistance last week, resuming its long-term uptrend with mild upside acceleration evident in D MACD. The clean breakout validates the bullish structure that has been building for months and sets the stage for further gains.

Near-term outlook will stay bullish as long as 44,789.03 support holds. The next major hurdle comes at 61.8% projection of 28,660.94 to 45,073.63 from 36,611.78 at 46,753.38. This level is in proximity to the upper boundary of the long-term rising channel, implying strong resistance could be seen on the first approach.

However, sustained break above this Fibonacci level, coupled with a decisive break of the rising channel ceiling, could prompt medium-term upside acceleration. Such a scenario would open the door for DOW to push beyond the psychological 50,000 mark toward 100% projection at 53,022.13.

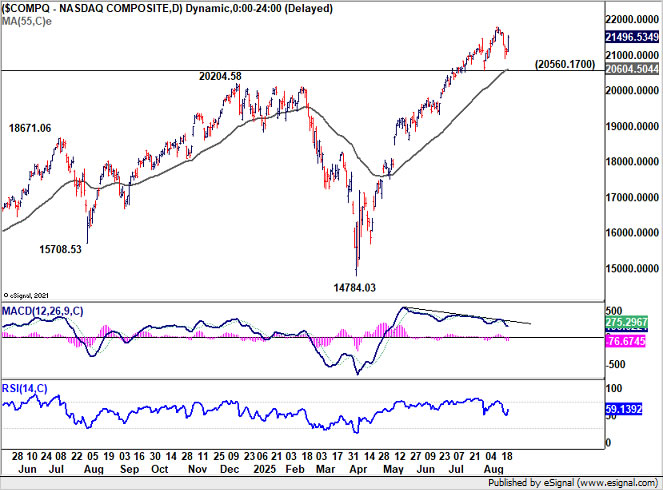

NASDAQ also held up despite a sharp intra-week slump. Downside was contained well above 20,560.17 support, keeping the near-term uptrend intact. The key question now is whether the index can muster enough momentum to break decisively through its own long-term channel resistance. If it succeeds, the path for NASDAQ would be open toward 100% projection of 10088.82 to 20204.58 from 14784.03 at 24899.78 as next medium term target.

Dollar Index, meanwhile, looks increasingly vulnerable. Price action from 96.37 is still viewed as a corrective pattern that could extend. A bounce back toward 100.25 cannot be ruled out. But rejection at 55 D EMA keeps near-term bias tilted lower. The broader risk lies to the downside.

With risk appetite strengthening and equities breaking higher, Dollar Index could soon crack below 96.37 support, confirming resumption of the broader decline from 110.17. That would also threaten the long-term channel that has defined the uptrend since 2008 low at 70.69. Sustained break of the channel would signal the start of a medium-to-long-term downtrend toward levels below 90.

EUR/USD Eyes Structural Test on Policy Divergence

Fed’s dovish tilt and Dollar Index’s vulnerability are not happening in isolation. Developments in Europe are also shaping the outlook, with Eurozone resilience and ECB’s pause in easing adding another additional pressure on the greenback.

Last week’s Eurozone data strengthened the case that ECB is now firmly in a prolonged pause. Even if the easing cycle might not have fully ended, there is little urgency to deliver further cuts. As the Fed edges closer to rate reduction, this divergence lends EUR/USD a supportive backdrop.

Eurozone’s August PMI reports provided a boost to sentiment. Manufacturing returned to expansion, while services held resilient despite trade frictions and tariffs. The data suggest that Eurozone businesses are coping better than expected with both global and domestic headwinds.

Wages development in Eurozone also remain a key factor. Negotiated pay jumped 3.95% yoy in Q2, up sharply from 2.46% in Q1. While below the peak 5.4% rate of 2024, the rebound underscores the persistence of domestic cost pressures. This stickiness ensures ECB will remain wary of easing too far.

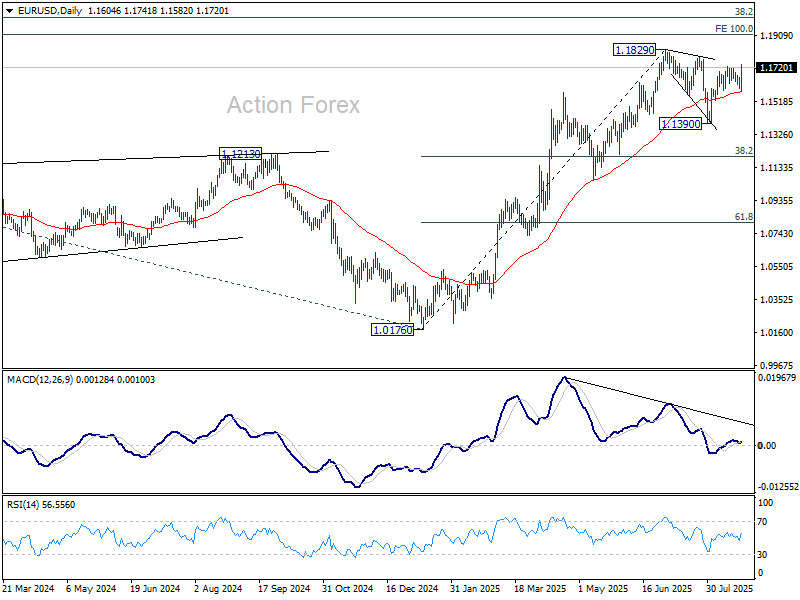

Technically, while EUR/USD’s pullback last week was slightly deeper than expected, the strong support from 55 D EMA affirms near term bullishness. The development is so far in line with the case that correction from 1.1829 has completed at 1.1390, and up trend from 1.0176 is ready to resume.

On break of 1.1829, EUR/USD will then be facing a key resistance zone at around 1.2, 38.2% retracement of 1.6039 (2008 high) to 0.9534 (2022 low) at 1.2019. Decisive break of 1.2 will bolster the case that EUR/USD is not just staging a cyclical rebound but is reversing a structural downtrend that has dominated for more than 15 years.

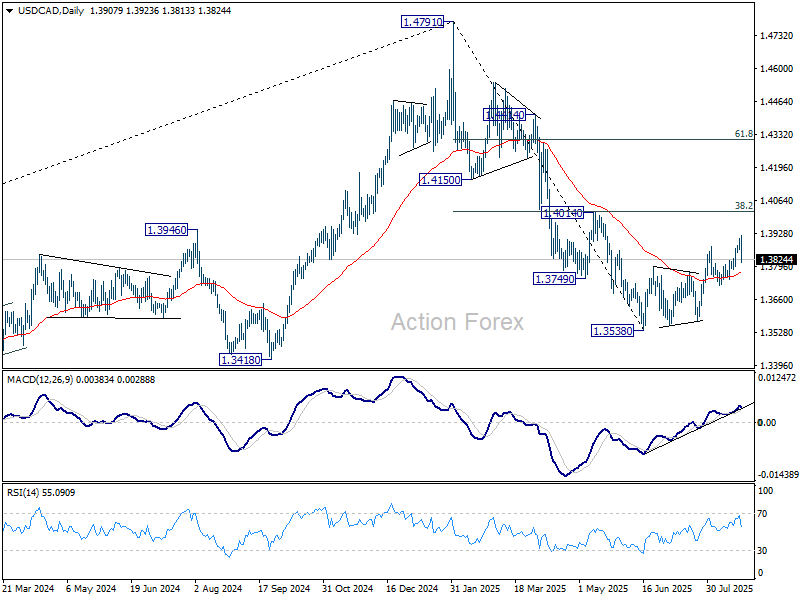

USD/CAD Weekly Outlook

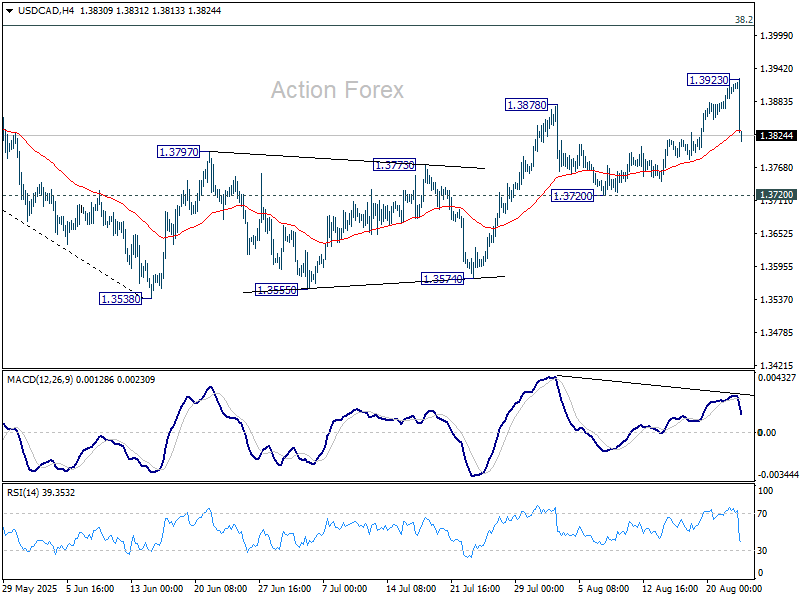

USD/CAD rose to 1.3923 last week but dived sharply from there. Initial bias is turned neutral this week first. Price actions from 1.3538 are seen as a corrective pattern. As long as 1.3720 support holds, another rise could still be seen. However, upside should be limited by 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017). Meanwhile, firm break of 1.3720 will argue that the corrective bounce has already completed, and bring retest of 1.3538 low.

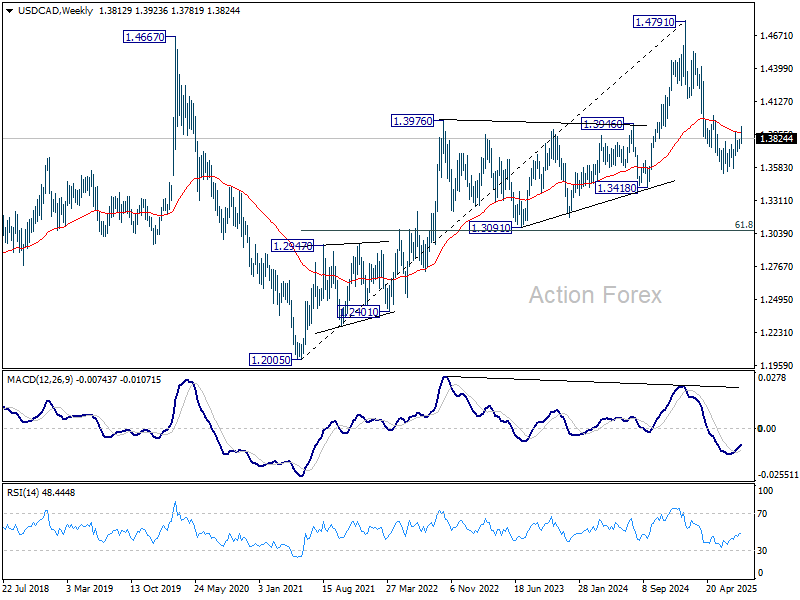

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

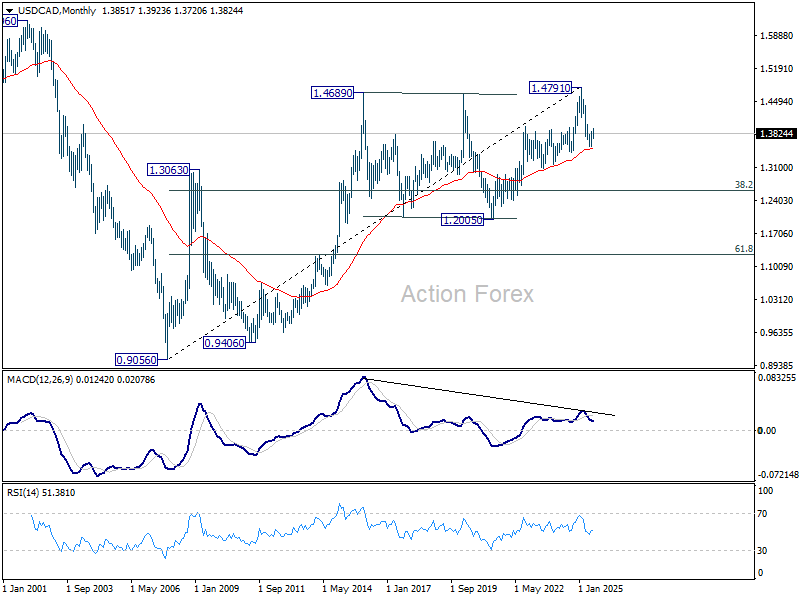

In the long term picture, as long as 55 M EMA (now at 1.3514) holds, up trend from 0.9056 (2007 low) should still resume through 1.4791 at a later stage. However, sustained trading below 55 M EMA will argue that the up trend has already completed, with rise from 1.2005 to 1.4791 as the fifth wave. 1.4791 would then be seen as a long term top and deeper medium term down trend should then follow.

[ad_2]

Source link