[ad_1]

We are concluding a fairly muted trading week, with participants usually taking the final trading week of August to reload their batteries before entering the volatile final four months of the year.

As a matter of fact, the session close will be essential to watch as month end flows tend to move markets quite largely.

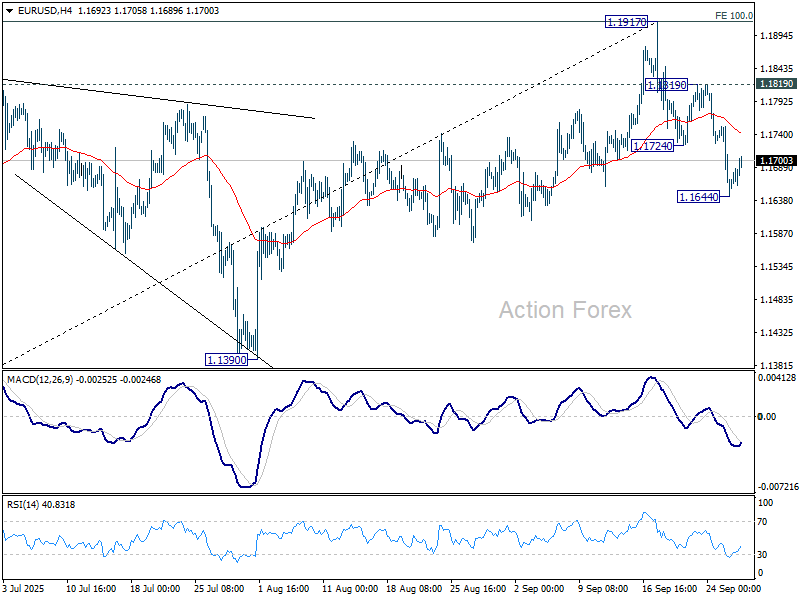

Indecisive trading, Ukraine-Russia talks take a step back

Markets decided to consolidate on relative low-volume trading.

Action in Forex markets was almost nonexistent, with low-volatility and volumes ranges, while equities went higher step by step.

The S&P 500 still reached some new all-time highs and the Dow Jones is holding above its previous record (Is a double top into work for the index? This could have big technical implications) – It isn’t shocking to get timid action ahead of Non-Farm Payrolls, particularly with the current state of things in Markets.

Jerome Powell is changing his tone, the Federal Reserve’s independence is getting challenged harshly, and diplomatic advances are failing: The German Chancellor Merz announced that Zelenskyy-Putin talks won’t take place anytime soon.

With the past month’s weak NFP report and a contradicting July PPI putting back tariff fears on the table, the path ahead is unclear yet again.

Weekly performance from different asset classes

Weekly Asset Performance, August 29, 2025 – Source: TradingView

Cryptocurrencies have seen quite a selloff this week, but this comes after a decent past week.

Nothing is too shocking here as volatility decreases and key data is expected next week.

However, some relatively weak highs have been formed, as can be seen in our past week’s analysis of the Cryptocurrency Market.

Indeed, Bitcoin has formed a double top and is failing to provide much to counter its effect, while Ethereum peaked at a new all-time high on Saturday before correcting further.

Ether has better prospects than its older brother, but its performance will still be contingent on BTC’s performance.

For the rest, Nasdaq and other stock indices weren’t performing much, but Nvidia earnings brought positive sentiment back.

The winners of this week are commodities, with Oil and Gold standing on top (Silver also had quite a strong performance). It seems that Powell’s pivot, although not having a big influence on other Markets, helped metals get back on their 2025 bull train.

We should get a better idea if that is to continue after next week.

Always keep an eye on the US Dollar to gauge the state of other markets (a strong USD usually leads to lower demand for Metals).

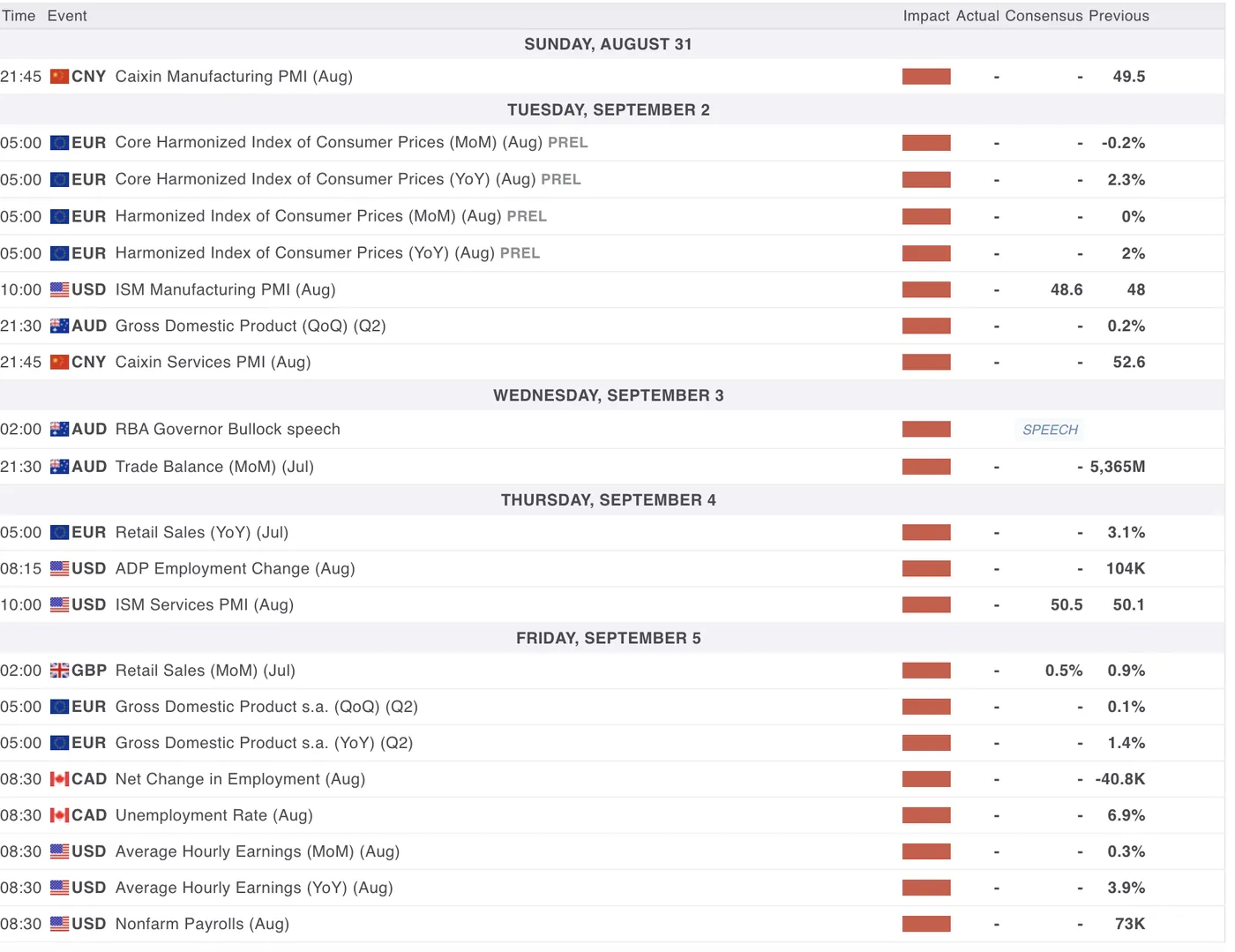

The Week Ahead – US Non-Farm Employment in focus (with some other key data points)

The beginning of next week should see volumes slightly getting back due to beginning of the month and quarter positioning.

However, the entire trading planet is awaiting for Friday’s Non-Farm Payrolls report, therefore trading won’t be as clear before that date.

Asia Pacific Markets – Growth data for Australia with Governor Bullock and PMIs for China

China and Australia will be in focus for APAC trading next week:

China opens the week with Caixin Manufacturing PMI on Sunday evening, a key gauge of factory activity that often sets the tone for Asia (and has high influence on AUD and NZD performance)

The Services PMI on Tuesday evening will complement the picture, amid a still slowing Chinese economy (most of the recent growth has been generated from government stimuli).

Australia’s week is also packed with data – Manufacturing PMIs and Q2 GDP land on Tuesday, giving insight into growth momentum.

Later, Thursday’s Trade Balance figures and comments from the Royal Bank of Australia Governor Bullock will add spice, with markets parsing every word for future policy hints – The RBA has just about one extra cut priced in for the year.

Japan and New Zealand won’t see much in terms of key data.

The Bank of Japan is the next APAC central bank to release their rate decision, with a pause mostly expected, but either way, the decision will not come before the middle of the month (September 18th).

The BoJ is trying to push back their hike (13% chance of a hike priced in for the year) and would, like US President Trump, love for the FED to cut to reduce the high interest rate differentials.

In terms of Asian Equity markets, the Nikkei and Hang Sang are both consolidating around their yearly highs in search of further momentum, while the Singapore STI, which reached a new record of 4,272 on Wednesday 13th has started to decline the past two days – is it profit-taking again or is Asian economic activity starting to get dragged by the Trump tariffs?

US, Europe and UK Markets – US NFP and Services PMIs, Eurozone Inflation and Canadian Employment

The week kicks off slowly for Markets, but really starts to pick up on Tuesday with Eurozone inflation data.

Core CPI is expected to stay soft at 2% YoY, while monthly numbers remain flat – with European inflation hanging around 2%, the European Central Bank should hold still for a while now.

A very small 10 bps cut premium is priced in for the rest of the year, but except for a sudden fundamental change, the ECB Main policy rate should stay between 2% to 2.15%.

In the UK, attention turns to Friday with Retail Sales (expected +0.4% MoM), a release that could give the Pound some direction after a quiet stretch. A weak number would reinforce the idea that consumer demand remains fragile, while a beat may push back some dovish expectations from the Bank of England.

For North America and actually for all markets, the spotlight is firmly on the US labor market.

Thursday’s ADP Employment Change will provide a first look, before Friday’s Nonfarm Payrolls report sets the tone. Markets expect around 78k jobs added – downward revised expectations after the prior month surprise revisions.

The US unemployment rate is still only at 4.2%!

Alongside payrolls, Average Hourly Earnings will be crucial to gauge wage pressures.

Less influential but released at the same time, Canadian employment data (including unemployment, currently at 6.9%) could bring extra volatility to USDCAD.

Don’t forget the Canadian Trade Balance data, releasing on Thursday at 8:30 A.M.

Finally, don’t overlook PMI releases across the board – ISM Manufacturing on Tuesday, ISM Services on Thursday– all of which will feed into the global growth narrative.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (High-tier data only)

Safe Trades and enjoy your weekend!

[ad_2]

Source link